Facing foreclosure can feel overwhelming, especially when you don’t know how much time you have or what happens next. The uncertainty is often worse than the situation itself.

In most cases, lenders cannot begin foreclosure until a borrower is at least 120 days delinquent under federal mortgage servicing rules. However, the exact timeline can vary depending on your state and loan type.

This guide breaks down the foreclosure timeline step by step, so you understand exactly where you are, what comes next, and, most importantly, how you can still stop foreclosure, even if the process has already started.

Foreclosure Timeline Key Takeaways

Before diving into the details, here are the most important things to understand about the foreclosure process timeline:

- The foreclosure timeline typically ranges from 3 to 12+ months, depending on the state and process

- The process includes pre-foreclosure, notice of default, and auction stages

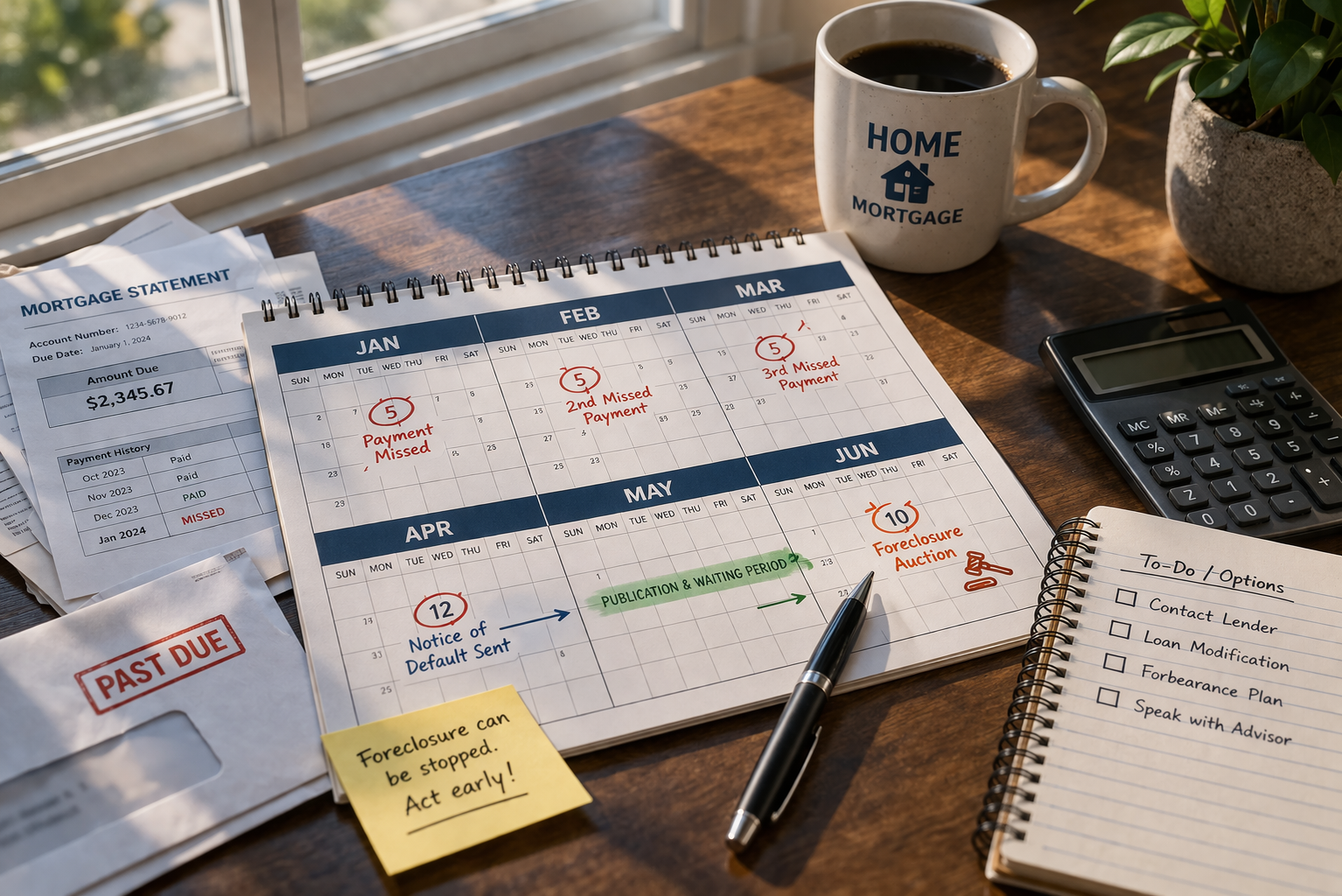

- Foreclosure usually begins 90+ days of missed mortgage payments, or about 90+ days of missed mortgage payments. The period before this is known as pre-foreclosure, where borrowers still have the most flexibility.

- A Notice of Default is typically issued after 90 days of missed payments and marks the official start of foreclosure proceedings.

- Homeowners can often stop foreclosure even after it has started

- Judicial states like Florida move more slowly, while non-judicial states like Texas move much faster

- Fast solutions, like a foreclosure bailout loan, can help stop foreclosure before auction

Quick Foreclosure Timeline Overview

The foreclosure process doesn’t happen overnight — but it can move faster than most homeowners expect, especially if action isn’t taken early.

The average foreclosure timeline depends on multiple factors, including state laws, lender behavior, and how quickly the borrower takes action. The foreclosure process timeline in the U.S. typically ranges from 3 to 12+ months.

In non-judicial states like Texas, foreclosure can happen in as little as 3–6 months because the process happens outside the courts. Judicial states like Florida, however, tend to take longer due to court involvement.

Here’s a simplified breakdown of the foreclosure timeline:

| Stage | What Happens | Typical Timeframe |

| Missed Payment | Loan becomes delinquent | Day 1–30 |

| Late Payments | Fees + lender contact | 30–90 days |

| Notice of Default | Formal foreclosure begins | ~90 days |

| Pre-Foreclosure | Opportunity to resolve | 3–6 months |

| Auction | Property sold | 6–12+ months |

Understanding where you are in this timeline is critical because your available options depend heavily on timing.

Stage 1: Missed Payments & Pre-Foreclosure

The foreclosure timeline starts the moment you miss your mortgage payment. At this point, you are not yet in foreclosure — you are in pre-foreclosure, which is often the most manageable stage.

Most lenders provide a short grace period before applying late fees, but the real escalation happens over time. After 30 days, your loan is considered delinquent. After 60 days, lender communication increases. By 90 days, the situation becomes serious enough to trigger formal action.

This early period is often called the mortgage delinquency timeline, and it is when lenders attempt to resolve the issue before pursuing foreclosure. Contrary to what many believe, lenders typically prefer to avoid foreclosure altogether due to the time and cost involved.

Understanding the difference between pre-foreclosure and foreclosure is essential. Pre-foreclosure gives you time, flexibility, and options. Once foreclosure begins, those options narrow — but they do not disappear entirely.

Stage 2: Notice of Default (Escalation Phase)

When a borrower falls significantly behind, the lender issues a Notice of Default (NOD). This is a formal legal document that signals the transition from pre-foreclosure into active foreclosure proceedings.

The notice of default timeline can vary slightly by state, but its meaning is consistent: the lender is initiating legal action to recover the property if the debt is not resolved.

At this stage, the situation becomes more urgent. Your credit is further impacted, and the lender may begin preparing for a foreclosure sale. However, you still have time to act.

One of the most important concepts here is the reinstatement period in foreclosure, which allows borrowers to bring their loan current by paying the overdue balance, fees, and penalties. This can stop foreclosure and restore the loan.

Other options may include negotiating with the lender, selling the property, or securing alternative financing. While these options become more time-sensitive, they are still very much possible.

Stage 3: Judicial vs Non-Judicial Foreclosure

Not all foreclosure timelines are the same. One of the biggest differences depends on whether your state uses judicial or non-judicial foreclosure.

In a judicial foreclosure, the lender must go through the court system to obtain approval before selling the property. This process is typically slower and more structured. Florida is a common example of a judicial foreclosure state.

In a non-judicial foreclosure, the lender can proceed without court involvement, based on the terms of the mortgage agreement. Texas is one of the most well-known non-judicial foreclosure states, and timelines there are significantly shorter.

| Feature | Judicial | Non-Judicial |

| Court required | Yes | No |

| Timeline | Slower (6–12+ months) | Faster (3–6 months) |

| Common States | Florida | Texas |

| Borrower Time | More time to act | Less time to act |

In the U.S., foreclosure laws are governed at the state level, which is why timelines vary so significantly. Judicial foreclosure states require court approval, while non-judicial states allow lenders to proceed based on contractual agreements. This legal distinction is one of the most important factors influencing how long foreclosure takes.

| Foreclosure Type | States |

| Judicial Foreclosure States | Florida, New York, New Jersey, Illinois, Pennsylvania, Ohio, South Carolina, Wisconsin, Indiana, Louisiana |

| Non-Judicial Foreclosure States | Texas, California, Georgia, Arizona, Nevada, Washington, Oregon, North Carolina, Tennessee, Missouri |

| Mixed / Hybrid States (both processes may apply depending on loan terms) | Alabama, Colorado, Michigan, Minnesota |

Stage 4: Foreclosure Sale / Auction

If the issue is not resolved, the foreclosure process moves to its final stage: the foreclosure auction. The period right before the foreclosure auction is often the last realistic opportunity to stop foreclosure.

The foreclosure auction process begins when a Notice of Sale is issued, setting a specific date for the property to be sold. At this point, timelines become extremely tight, and options become more limited.

At the auction, the property is sold to the highest bidder. This could be an investor or, in some cases, the lender itself.

| Outcome | What It Means |

| Sold | Ownership transfers to a new buyer |

| Not sold | Property becomes REO (bank-owned) |

What Happens at a Foreclosure Auction?

A foreclosure auction is the final step in the foreclosure timeline, where the property is sold to recover the unpaid mortgage balance. These auctions are typically held by the county, a trustee, or a court-appointed official, depending on whether the foreclosure is judicial or non-judicial.

Before the auction takes place, the lender sets a minimum bid — usually equal to the outstanding loan balance, plus fees and legal costs. This is known as the opening bid.

During the auction:

- Buyers place bids, often in cash or with pre-approved financing

- The highest bidder wins the property

- Payment terms are typically strict and time-sensitive

In many cases, especially when the opening bid is high, the property may not sell. When that happens, ownership transfers back to the lender, and the property becomes what is known as a real estate owned (REO) property.

To sum up:

- At a foreclosure auction, the property is sold to the highest bidder, often to investors or the lender itself.

- If a home does not sell at auction, it becomes bank-owned and may later be listed for sale on the market.

- Foreclosure can sometimes be stopped even days before the auction, but action must be immediate.

Can You Stop Foreclosure at Each Stage?

Most homeowners assume foreclosure becomes inevitable at a certain point — but that’s not always true. In reality, foreclosure can often be stopped at multiple stages.

| Stage | Can You Stop Foreclosure? | Options Available | Difficulty Level |

| Missed Payments | Yes | Catch up payments, repayment plan | Easy |

| Notice of Default | Yes | Reinstate the loan, negotiate | Moderate |

| Pre-Foreclosure | Yes | Sell, refinance, or bailout loan | Moderate–High |

| Pre-Auction | Sometimes | Fast financing, legal delay | High |

| Last-Minute | Rare but possible | Emergency funding | Very High |

Even at later stages, foreclosure is not always irreversible. In many cases, lenders are primarily focused on recovering the loan balance — not taking ownership of the property. That means solutions are often still available, especially if action is taken quickly.

If you are exploring the best foreclosure bailout loan options or looking for ways to stop foreclosure fast, timing becomes the most important factor. Foreclosure can often be stopped later than most homeowners expect, but waiting reduces your chances significantly.

How Long Does Foreclosure Take?

On average, foreclosure takes between 3 and 12+ months in the U.S., depending on state laws and borrower action. The faster a borrower responds, the more likely the timeline can be extended or stopped.

Keep in mind that the foreclosure timeline is not fixed. It depends on state laws, lender behavior, and how proactive the borrower is during the process.

In judicial states like Florida, foreclosure can take a year or longer due to court involvement and case backlogs. In non-judicial states like Texas, the process can move much faster — sometimes in just a few months.

Delays, negotiations, and proactive action can extend the timeline. In contrast, inaction can accelerate the process significantly.

What to Do If You’re Facing Foreclosure

If you are currently in the foreclosure timeline, the most important step is to act quickly.

Many homeowners wait too long to respond, hoping the situation will improve. In reality, early action significantly increases your available options.

Start by understanding where you are in the process. Then explore all available solutions, including working with your lender, selling the property, or securing alternative financing.

Foreclosure is often preventable with the right strategy and timing — but delays reduce your chances of success. The key is to move from uncertainty to action as soon as possible.

Below are the most common and effective options homeowners use to stop or avoid foreclosure:

- Catch up on payments

- Negotiate with your lender

- Sell your property before foreclosure

- Use a foreclosure bailout loan

If you’re exploring solutions, it’s also important to learn how to avoid foreclosure rescue scams, especially when dealing with urgent offers that seem too good to be true.

Catch Up on Payments or Negotiate With Your Lender

One of the most straightforward ways to stop foreclosure is to bring your mortgage current. This may involve paying the missed payments in full or working out a repayment plan with your lender.

Lenders often prefer to work with borrowers rather than complete a foreclosure, since foreclosure is costly and time-consuming. Many lenders offer solutions such as loan modifications, forbearance agreements, or structured repayment plans — especially if you act early in the process. These options are more likely to be available during pre-foreclosure or shortly after a Notice of Default is issued.

However, this option may not be realistic if the missed payments have accumulated significantly or if your financial situation has changed long-term. In those cases, alternative solutions may be necessary.

Sell Your Property Before Foreclosure

Selling your home before the foreclosure auction is another viable option, especially if you have equity in the property.

This allows you to pay off the loan balance, avoid foreclosure on your record, and potentially walk away with remaining funds. Even if you owe more than the home is worth, a short sale may be possible with lender approval.

You can usually sell your home during foreclosure up until the auction date, depending on state laws.

This option requires time, coordination, and a buyer, which can be challenging if you are already late in the process. That’s why many homeowners explore faster alternatives if the timeline is tight.

Use a Foreclosure Bailout Loan to Stop the Process Fast

Foreclosure can often be stopped even close to the auction if fast financing is secured in time. For homeowners who are short on time, have poor credit, or have been denied by traditional lenders, a foreclosure bailout loan can be one of the most effective solutions.

These loans are specifically designed to pay off your existing mortgage quickly, stopping the foreclosure process and giving you time to stabilize your situation.

Unlike traditional loans, these solutions are often based on the value of the property rather than your credit score or income history. This makes them especially useful for borrowers who feel like they’ve run out of options.

If you are exploring ways to stop foreclosure fast or comparing the best foreclosure bailout loan options, acting quickly is critical. The closer you are to auction, the fewer options remain — but the right solution can still make a difference.

Stop Foreclosure Fast With Hard Money Loan Solutions

If you’ve been denied by banks, feel like you’re out of time, or believe your credit is too damaged — you are not alone. This is exactly where we help.

At Hard Money Loan Solutions, we specialize in helping homeowners stop foreclosure quickly, even when traditional lenders say no.

We do not rely on credit scores the way banks do. We do not require extensive income verification or complicated financial documentation. Instead, we focus on speed, flexibility, and real solutions.

Our foreclosure bailout loan programs are designed specifically for urgent situations. Whether you are in pre-foreclosure or just days away from auction, we can move quickly to help you regain control.

Many of our clients come to us after being turned away elsewhere. They’ve been told it’s too late or that their credit disqualifies them. But the reality is — solutions still exist.

If you are searching for the best foreclosure bailout loan option or need to act immediately to protect your property, our team is here to help.

When it comes to foreclosure, time matters more than credit score. The sooner you act, the more options you have. Apply for our loan now!

Conclusion: Understanding the Foreclosure Timeline Gives You Control

The foreclosure process can feel overwhelming, but it becomes much more manageable once you understand how the timeline works.

From the first missed payment to the final auction, each stage presents different risks — but also different opportunities to take action. The key is recognizing that foreclosure is not immediate, and in many cases, it is not inevitable.

The earlier you act in the foreclosure timeline, the more options you have — but even late-stage foreclosure can sometimes be stopped with the right approach.

Whether you choose to work with your lender, sell your property, or explore financing solutions, the most important step is to take action before time runs out.

If you are currently facing foreclosure, focus on where you are today — and what you can do next. Because even in difficult situations, solutions are often closer than they appear.

Foreclosure Timeline FAQs

Yes, foreclosure can often be stopped at multiple stages, especially with fast financing or repayment solutions.

Foreclosure is typically triggered after 90+ days of missed mortgage payments.

Yes, homeowners can usually sell their property before the auction to avoid foreclosure.

The lender begins formal proceedings and sets a timeline toward a foreclosure sale or auction.

{kind=link}